14 Sep Did you know: the difference between common financial attachments (Part One) by Shauna O’Toole, MA, CFRE

Did you know that budgets and financial documents are often the first things a grant reviewer will read when considering an organization’s proposal? Sometimes grant professionals leave attachments and budgets for the end, perhaps because these documents can be confusing or intimidating to those of us without an accounting background. This two-part guide will help you correctly identify which attachment the funder is requesting and explain why it is helpful for the funder to have the information contained in each document.

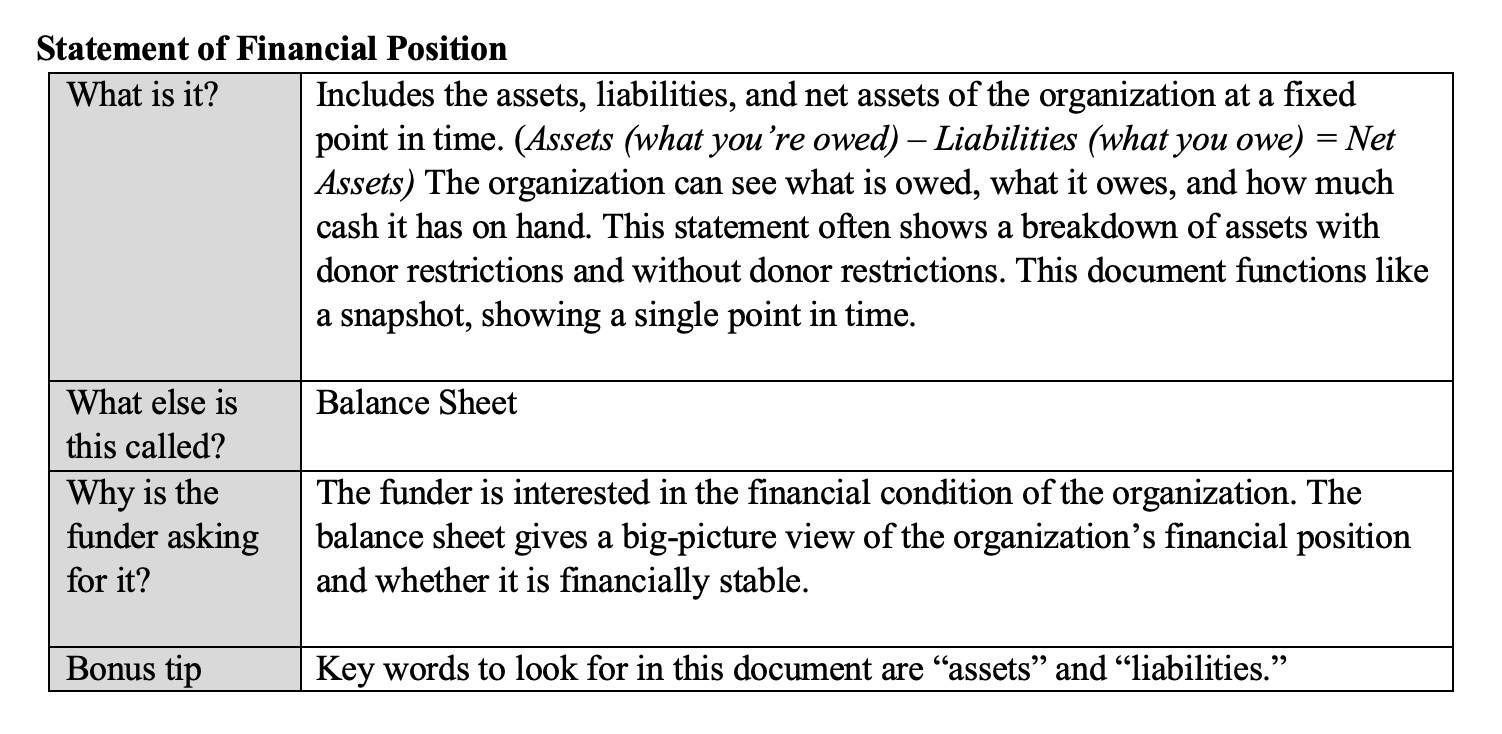

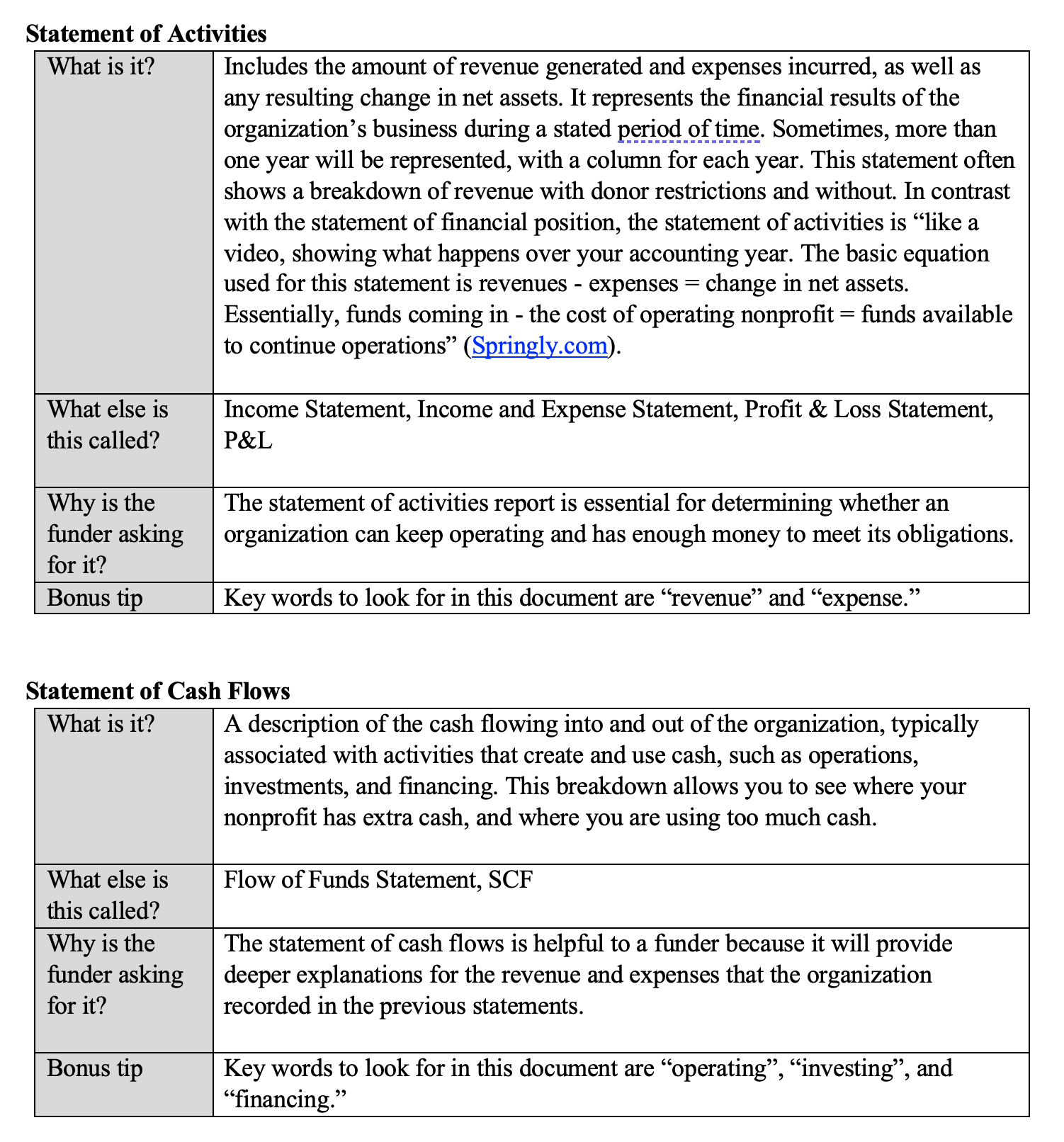

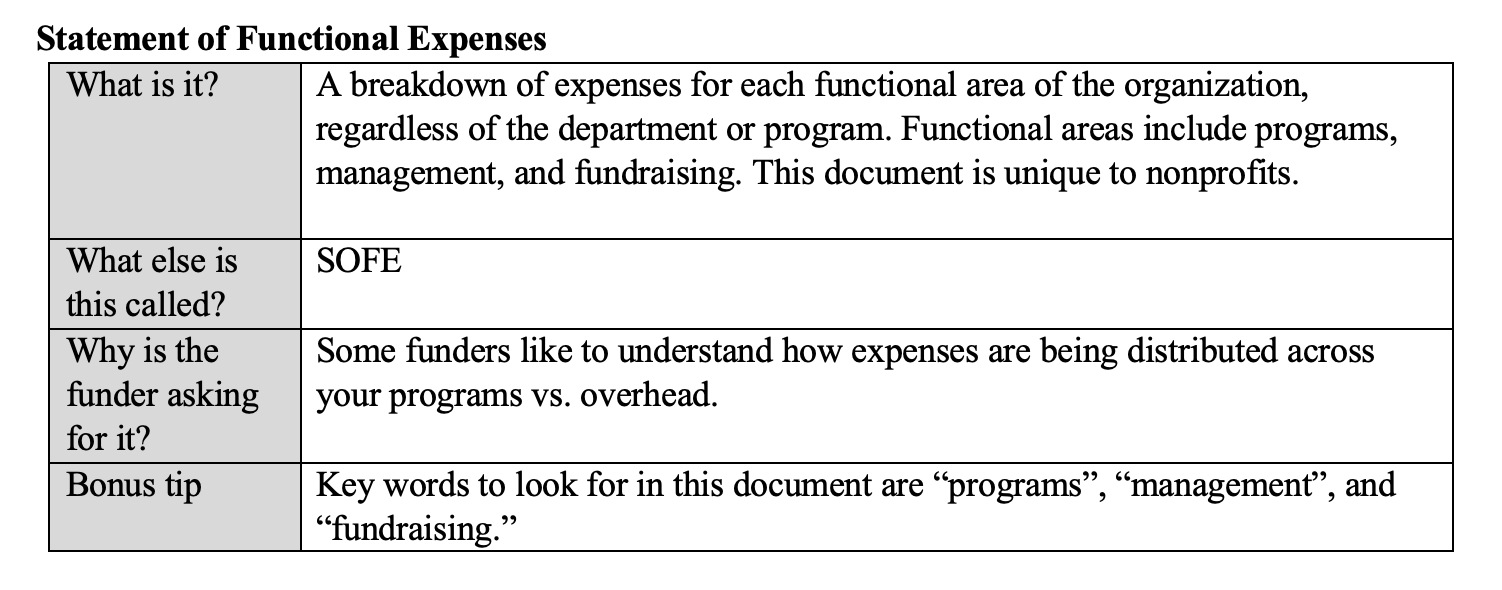

Financial statements: The following four documents, collectively, are often referred to as “financial statements” or “financials.” Complete year-end versions of each document are typically available within three months of the close of the fiscal year. If the most recent year-end document is outdated or the funder asks for a current statement, your finance professional should produce a year-to-date version to include alongside the outdated annual version. Year-to-date financials should be dated within three months of the grant submission date.

Keep in mind that the required attachments will vary slightly from proposal to proposal. A savvy grant professional will always seek out the funder’s specific format and guidance. Now that you have a grasp of financials, stay tuned for Part Two, where we will cover budgets and other commonly requested attachments, like the IRS Form 990 and audit.

Do you need more support with financial attachments? AGS offers professional development webinars that align to GPCI’s competencies and skills. They address multiple skills within a competency, interrelated skills across competencies, or a specific skill within a competency in great detail. All of our courses:

- Align with GPCI competencies;

- Are approved for CEUs by GPCI and CFRE International; and

- Are led by nationally recognized GPA-approved trainers.

This BLOG is aligned with the Grant Professional Certification Institute’s Competencies and Skills

Competency #2: Knowledge of organizational development as it pertains to grant seeking.

Skill 2.1: Assess organizations’ capacity for grant seeking.

Competency #3: Knowledge of strategies for effective program and project design and development

Skill 3.3: Identify strategies for educating key personnel about financial and programmatic accountability to comply with funder requirements

Sources and Additional Resources:

https://www.accountingtools.com/articles

https://www.jitasagroup.com/jitasa_nonprofit_blog/nonprofit-audit/

https://www.jitasagroup.com/nonprofit-resources/nonprofit-accounting-terms/

https://www.springly.org/en-us/blog/essential-nonprofit-financial-statements/#income

and https://www.araize.com/statement-of-activities-report/